How are sanctions created? Overview on the example of the European Union

Even if it turns out later in the proceedings that you have behaved correctly, it is in no way reasonable to attract such negative media coverage; as well as experiencing the stress and resource consumption inevitably associated with such procedures. Therefore, it is always wise to prevent problems and look for solutions to mitigate such risks as early as possible, which AS Creditinfo Eesti can always help you with.

However, how are restrictive measures established, who is responsible for the fact that the EU can put someone on its lists at all, and is it inevitable to be on the sanctions lists or is it possible to get out of there somehow? Let’s take a closer look at this process here.

Initiation of sanctions in the European Union

The European Union is an association of independent countries operating on the basis of its founding treaty(s). One of the important principles is that the European Union has a common foreign and security policy, one of the important parts of which is, among other things, the imposition of sanctions in situations where it is desired :

- protect EU values, fundamental interests and security

- keep the peace

- consolidate and support democracy, the rule of law, human rights and the principles of international law

- prevent conflicts and strengthen international security

We have already covered the nature of sanctions and their relevance in relation to the situation in Ukraine in more detail on the Creditinfo channels beforehand, so we would currently only look at the process of how the idea of sanctioning at the EU level results in a mandatory legal act for all persons operating on the territory of the Community.

The creation of legislation necessary for the implementation of sanctions can be viewed at the EU level in three different aspects :

- Legislation to take over UN sanctions is being created

- Legislation is being created to implement UN sanctions in an expanded form

- Legislation to establish autonomous EU sanctions regimes.

The European Foreign Service (institutionally part of the European Union Commission) is responsible for the implementation of EU sanctions policy , whose responsibility is to prepare drafts for establishing or changing sanctions regimes.

Of course, this is done in close cooperation with the member states, for example it is very important to get input regarding the identifying data of sanctioned persons, which information is often available to national specialists, and including it in the legislation establishing the sanction (or its annex) will help to significantly reduce the number of false positive responses arising from the implementation of the legislation in the future.

Since all member states must give their consent to the imposed sanctions, the draft sanctions move to the institution with the member states’ representation, i.e. the Council of the EU. The next instance is therefore the corresponding working group of the Council of the European Union (RELEX) , where the specialists of the member states cooperate to reach an agreement on the text of the legislation.

If agreement is not reached, the agreement will continue in the working group formed by the permanent representatives of the member states at the EU (COREPER) , from there the draft will go to the General Assembly of the Council of the EU (forum of heads of government), where it will be adopted and the text of the legislation will be agreed upon. For mandatory compliance, the legislation will be in the EU gazette after its publication.

Ending sanctions

Existing EU autonomous sanctions legislation is reviewed regularly, but no less often than once every 12 months.

Since the EU follows the principles of the rule of law (Rule of Law), it is of course also possible for persons under sanctions to get rid of the status of a sanctioned person through legal processes.

There are two main options for this – to publish a motivated statement of wish to this effect directly to the Council of the EU, which will then process the corresponding application and make a decision regarding whether to leave the sanctions list or to remove it from it, or another, more widely used option, to turn to the General Court of the European Union ( General Court of the European Union).

For example, at this point it is perhaps even appropriate to bring up the most talked about decision of recent times about the victory achieved by Violetta Prigozhin, the mother of the late Yevgeni Prigozhin, regarding her delisting .

AS Creditinfo Eesti has continued to take on the concern of providing the necessary support to market participants in the implementation of international sanctions, and we are ready to help with various issues, both with advice and force. We believe that in this way, in cooperation with our customers, we can best contribute to the achievement of the common foreign and security policy goals of the EU.

Visit: creditinfo.ee

Webinar: Baltic Market Overview

Register and join Jekaterina Rojaka, COO Creditinfo Lietuva , as she hosts another session on the Baltic market overview.

During this session, you will get the latest updates on the following:

- Improving sentiments – will it strengthen economic growth?

- Rising interest rates – what is the impact on the market?

- Sectoral perspective – losers and winners

Please complete the registration form below to receive the event link. The session will be in English – http://ow.ly/MSjh50NHVVX

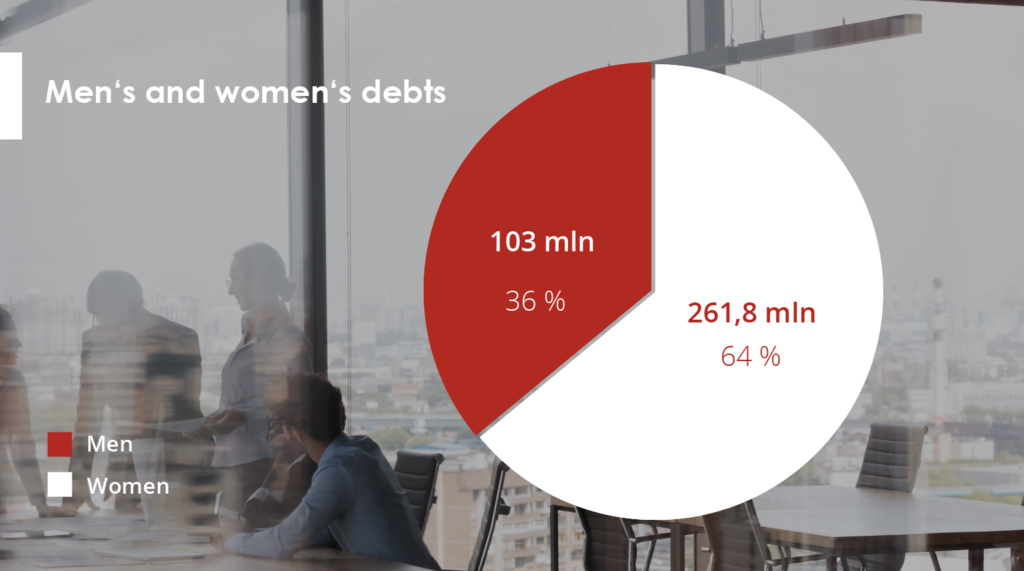

Lithuanian debts increased by €6.8 million since the beginning of 2023

According to Creditinfo Lithuania’s latest analysis, Lithuanian debts have increased by €6.8 million since the beginning of the year, reaching a total of €364.8 million.

Of this amount, male’s debts stand at €261.8 million, while female’s debts are at €103 million. This is almost €6.8 million more than at the beginning of this year (€358 million). The total number of borrowers has also risen by 5,000 in the first quarter of this year, with the current total standing at almost 201,000.

Creditinfo Lithuania has recorded almost 201,000 debtors in its systems for March, with a total of 235,300 individuals having 235,300 debts in Lithuania.

After a more detailed examination of the debtor data, it was found that over 129,000 males and 72,000 females are currently in debt, making up 64% and 36% of all debtors respectively. Additionally, 32,500 males and almost 20,000 females have multiple debts, with 25.3% of male debtors and 27.7% of female debtors holding two or more debts.

On average, males owe €2,029, which is 30% more than the average debt owed by females (€1,435). This trend, coupled with the higher number of male debtors, results in men holding 78% of the total debt amount, while women hold only 22%.

During the first quarter, an additional 5,000 individuals in Lithuania fell into debt.

In March, the total number of individuals in debt amounted to 201,000, marking an increase of 5,000 from January’s 196,000. The total value of debt owed by all debtors also rose from €358 million to €364.8 million, with the total number of debts recorded in the credit bureau system increasing by 5,300. The largest number of new debts to households registered in the first quarter of this year, after debts to the financial sector, were for utilities and energy, with a total of 1,518 debts (12%).

“The analysis suggests that the majority of new debts recorded this year can be attributed to the energy and heat price crisis. Rising fuel costs have resulted in increased indebtedness, with people seeking short-term financing in order to balance consumption and expenses,” explains Aurimas Kačinskas, the Head of Creditinfo Lithuania. “Not everyone has had sufficient time to alter their financial habits, which has resulted in the growing number and value of debts.”

Men aged between 35 and 45 are considered to be the most high-risk debtors

Despite fluctuations in the number of borrowers and their levels of indebtedness, the typical borrower profile has remained consistent in recent years. Men aged 35-45 are the riskiest debtors, with debts amounting to €75 million, accounting for almost 29% of the total amount owed by men. The second riskiest group is men aged 45-55, with €61 million in debt, representing 23.3% of the total amount owed by men. In third place are men aged 25-35, who hold €55 million in debt, accounting for 21% of the total amount owed by men. Men aged 55-65 hold €43 million in debt, while those over 65 hold €17 million. Men under 25 hold the lowest amount of debt at almost €15 million.

Among female debtors, the under-25 age group has the lowest amount of debt, while other age groups have the following distribution: €29 million (45-55), €26 million (35-45), €20 million (55-65), and €17 million each (25-35 and over 65).

According to Mr Kačinskas, it is important for citizens to assume their financial obligations responsibly and meet them on time to maintain a positive credit history, which determines their access to financial services, loans, credit cards and payment provisions.

One of the safest businesses in Lithuania – Dental Services

The profitability of some companies is almost half their revenues, very few go bankrupt.

Vilnius, Lithuania 06/02/2023. Although most dental businesses are small and usually employ fewer than 10 people, this is one of the most stable businesses in Lithuania. Profitability often exceeds one-third of income and only a few become insolvent. Dental businesses are 7 times less likely to go bankrupt than the average insolvency across all other businesses, according to an analysis conducted by Creditinfo Lithuania.

According to data from January 2023, there are currently almost 2,000 dental businesses in Lithuania employing 9,500 people. The number of companies and their employees is growing year on year. Dental businesses are generally small, with more than half of them employing fewer than 10 people. Only 12 organisations have created more than 50 jobs, while the largest dental service companies are Vilnius University Hospital (293), SB Dental Clinic (168), Denticija (153), Smile Academy (126), Smile Laboratory (124), Vilnius Implantology Centre Clinic (93), Panevėžys City Dental Clinic (72), Laudenta (71), Pasirink (66) and Žvėrynas Dental Clinic (59).

Revenues grow year on year, profitability remains high

Despite the pandemic’s restrictions on the medical services sector between 2020 and 2021, the total revenue of dental companies has grown consistently year on year, reaching €294.6 million in 2021, an increase of 39.8% compared to 2020 (€210.7 million), which in turn is an increase of 76% compared to 2019 (€167 million).

The top 10 companies with the most revenue in 2021 are SB Dental Clinic (€8.2 million), Vilnius Implantology Centre Clinic (~€7 million), Denticija (€3.2 million), Smile Academy (€3.1 million), Prodenta (€3.1 million), Žvėrynas Dental Clinic (€3 million), Sveikatos Gija (€2.9 million), Šiauliai Implantology Centre (€2.8 million), Laudenta (€2.6 million) and Dental Harmony (€2.6 million).

Dental service companies are characterised by relatively high profitability, reaching up to 45%. The top ten companies with the highest profits in 2021 are Laudenta (€922 thousand), SB Dental Clinic (€917 thousand), Implantera (€739 thousand), Šiauliai Implantology Centre (€713 thousand), Smile Design (€688 thousand), Vilnius Implantology Centre Clinic (€644 thousand), Klaipėda Orthodontics Centre (€592 thousand), Dantima (€556 thousand), Donatas Jurgaicis Odontology Clinic (€529 thousand) and Teeth Centre (€512 thousand).

“The dental services business has advantages – patients usually pay for services immediately, which speeds up the turnover of funds. In addition, some dental services are subject to significant VAT exemptions, which reduces the tax burden and increases the profitability of the companies,” says Jekaterina Rojaka, Head of Business Development and Strategy at Creditinfo Lithuania.

However, not all companies were profitable, with 148 dental service providers declaring a loss in 2021, compared to 128 in pandemic year 2020 and 133 in pre-pandemic year 2019.

Dentists 7 times less likely to go bankrupt

The dental services sector has a particularly low risk of bankruptcy compared to all other sectors, with 1% of firms currently at high risk of bankruptcy and 0% at the highest risk. The high and highest risk classes for late payment are 3% and 2% of companies, respectively. The riskiness of dental firms was slightly higher at the beginning of 2021, with 4% of firms in the high bankruptcy risk class (none in the highest) and 11% in the high and highest delayed payment risk classes.

No dental companies went bankrupt in 2021 or 2022, while 26 firms have become insolvent since 2003, an average of 1-2 per year.

The dental business is characterised by a low level of debt. As of January 2023, there were 98 registered debts in the credit bureau’s system, totalling €95 thousand. The average debt was €971.

Compared to companies operating in other sectors in Lithuania, dental service companies are 7 times less risky. For example, in January this year, 1.3% of dental businesses were classified as high and highest risk, compared to an average of 9.5% for all other businesses in Lithuania. In terms of the risk of late payment, 4.5% of firms were in the high and highest risk classes, while the average for all other firms was 17.2%.

Almost a fifth of dental businesses (359) have not yet submitted their financial statements for 2021.

More information:

Jekaterina Rojaka, Head of Business Development and Strategy, Creditinfo Lithuania (jekaterina.rojaka@creditinfo.com)

Travel agencies in Lithuania are slowly rising from the ashes

Revenues doubled in a year but remained three times lower than before the pandemic.

Vilnius, Lithuania, 24/01/2023. Travel agencies in Lithuania that declared their income in 2021 earned almost twice as much as in the previous year. However, compared to income in 2019, they earned almost three times less, according to an analysis carried out by the credit bureau Creditinfo Lietuva. Almost 100 tourism companies were loss-making. With the increase in travel flows, the number of debts increases and their average size grows.

There are currently 783 companies in Lithuania for which tour organisation is the main activity. In 2021, travel agencies declaring revenues collectively earned more than €171 million, almost double (82%) the pandemic year 2020 (~€94 million). However, travel agencies are still a long way from a real recovery – for example, in 2019, their revenues were almost €474 million, but fell more than fivefold in the aftermath of the pandemic.

According to 2021 data, the largest annual revenue was earned by the following companies: Novaturas (€108,995 million), Tez Tour (~€60 million), Itaka Lietuva (€12.5 million), Coral Travel Lithuania (€9.5 million), Kidy Tour (€8.9 million), Estravel Vilnius (€6.3 million), Estekspress (€4 million), Traveldeals LT (€4 million), Glotera (€3.6 million) and ZIP Travel (€2.9 million).

The top ten most profitable travel agencies are Novaturas (€909 thousand), Baltic Tours Group (€633 thousand), Vestekspress (€530 thousand), Glotera (€336 thousand), Traveldeals LT (€307 thousand), Baltic Clipper (€288 thousand), Baltic Travel Service (€271 thousand), TEZ Tour (€215 thousand), Estravel Vilnius (€158 thousand), Riviera Tours (€148 thousand) and ZIP Travel (€123 thousand).

Staff numbers shrink by a quarter

In total, travel agencies currently employ almost 2,000 employees (1,850). While the number of enterprises has remained almost constant over the past few years (776 in 2019, 787 in 2021), the number of employees has fallen by almost a quarter since 2019, from 2,426 to 1,850.

Travel agencies are more often headed by women, accounting for almost 56% of all managers. The average age of a travel agency manager is 49 years and the average age of a travel agency is over 15 years.

In the travel sector, men’s salaries are higher than women’s – as of November 2022, the average salary for men was €2,659 per month, while for women it was €2,014 per month. At the start of 2022, the average salary for women was €2,053 per month and for men was €2,364 per month.

State support has prevented more bankruptcies

Since 2004, a total of 94 travel agencies have gone bankrupt in Lithuania, with the highest number of bankruptcies recorded in 2009 (10) and in 2015 (12). In 2022, there were 5 travel agency bankruptcies, while there were 3 in 2021 and 4 in 2019. No travel agency bankruptcy was recorded in pandemic year 2020.

“The travel sector was one of the hardest hit by the pandemic, along with hotels and restaurants. During the pandemic, when revenues from tour operators dropped fivefold, it was state support that saved the sector from bankruptcy,” explains Aurimas Kačinskas. But the challenges of the pandemic were replaced last year by new challenges – the war in Ukraine and the sanctions imposed on Russia have exacerbated the energy crisis, fuel prices have risen and many travel routes have been disrupted. The slower-than-expected recovery of the air transport sector, with a sharp increase in fares, is having a negative impact on the business of tour operators, preventing them from recovering faster.

According to the head of the credit bureau, it was state support that determined the stability of the number of enterprises and the discipline of submitting financial statements – compared to other sectors, only 90 travel agencies did not submit their financial statements for 2021, making them ineligible for state support.

However, a risk analysis of travel agencies shows that there have been both positive and worrying signs in the recent period. For example, as of January this year, 9% of companies were in the high and highest classes of bankruptcy, compared with 12% a year ago. In terms of delayed payments, 17% of companies are currently in the high and highest risk classes, down from 21% last year.

Compared to 2020 and 2021, the recent increase in debt is slightly higher and the average amount of debt per person is growing. At present, 306 debts have been registered in the credit bureau system, amounting to more than €349 thousand, with an average debt of €1,141. A year ago, the number of debts was 316, amounting to €351 thousand, with an average debt of €1,112. In January 2020, 255 debts amounting to €203 thousand were registered, with an average debt of €798. 335 travel agencies mostly owe money to Sodra (€3 million). The debt of 158 travel agencies to telecommunications companies amounts to €222 thousand. 8 travel agencies owe €74 thousand to financial companies.

“The tour operator business is recovering, but revenue growth is slower than expected in the wake of the pandemic due to the many geopolitical and economic shocks around the world. The tourism sector is currently encompassed by a number of risks, so it is advisable to keep a close eye on the changing financial indicators of partners organising the trips,” concludes the head of the credit bureau.

More information:

Aurimas Kačinskas, CEO of Creditinfo Lithuania (aurimas.kacinskas@creditinfo.com)

Creditinfo Lithuania invests 1 Million Euros in new Credit Bureau System

The credit bureau is carrying out strategical changes and gathering resources inside of the group of companies.

In implementation of the development plans and presentation of new services, the credit bureau “Creditinfo Lietuva“ informs having invested one million euro into a new information system of the credit bureau and that it is going to introduce several innovative products soon. The credit bureau is implementing strategical changes – it is gathering all the data resources and processes inside the group of companies “Creditinfo Lietuva“ for more effective administration.

Last March, “Levine Leichtman Capital Partners” (LLCP) became the new main shareholder of the group of companies “Creditinfo”. It announced its plans to grow and to expand the activities of credit bureaus in the international market and to invest into development of new data-based solutions. The investor with solid international business management experience focuses on the information technologies and automated solutions.

“We have a good possibility to start providing more new services in Lithuania (as in other advanced financial markets), to start providing more new services that would enable the creditors to make faster and more accurate decisions, and the consumers to receive financing more expeditiously, – says Mr. Aurimas Kačinskas, CEO of “Creditinfo Lietuva“. – The services of credit information, risk management and data analysis that we are providing demand for bigger collection of the resources in one place, thus, we have invested into development of the credit bureau’s system of a new generation, and we have expanded the available IT platform. This allows controlling quality of the services better, providing them continuously, and expanding the suggest scope of services by innovative products.”

Automated solutions and artificial intellect data services will be introduced

The services of “Creditinfo Lietuva“ that will be launched soon will help the clients to use more automated solutions and products of the credit bureau not only in Lithuania, but also in other countries, and to evaluate creditworthiness of borrowers, and to control the financing risks. It is planned to introduce the innovations in the first quarter of this year already.

The pending changes are the part of strategy of the new main shareholder of the group of companies “Creditinfo”, LLCP – to apply the international business management experience for the activities of credit bureaus in more than 30 countries. The company of private capital, “Levine Leichtman Capital Partners” operating for 38 years, is managing 14 investment funds and has invested into 90 companies in the United States of America (USA) and Europe.

The international group of companies “Creditinfo“ includes the credit bureau operating in Lithuania, “Creditinfo Lietuva“, that was established in 2000. The credit bureau has been collecting and managing the biggest data system on creditworthiness of the Lithuanian companies and residents, and providing services of credit risk management, rating creation and modelling for more than 20 years. The company has 43 employees and its annual income in 2020 amounted to 5,6 million euro.

More information:

Aurimas Kačinskas, CEO of “Creditinfo Lietuva”

Aurimas.Kacinskas@creditinfo.lt

Tel: +370 618 10110

Average pay for women grows in Lithuania

The average pay for women has grown in 56 sectors after starting releasing information on gender pay gap. Within a matter of three months women’s average monthly pay increased by EUR 20, compared against an EUR 15 increase for men.

After Sodra (Lithuanian Social Security Authority) started publishing sectoral data on average gender pay gap, women’s average pay has grown in 56 sectors out of 81 within the past three months. Women’s monthly average pay increased from EUR 2 to EUR 325 in various sectors. In 13 sectors women’s pay grew by over 10% despite some economic activities where gender pay gap continued to grow for men, these are: insurance, re-insurance, pension accumulation companies, power generation, gas and air conditioning companies, and the pharmaceutical industry.

According to the analysis conducted by Creditinfo Lithuania, from April to July women’s average pay grew from 0.1% to 36.1%, or from EUR 2 to EUR 325 per month. In thirteen business sectors, women’s pay increased by over 10%, with the most remarkable growth reported in accommodation (16.8%), catering and supply of beverages (21.6%), gambling or betting industry (36.1%).

An increase from 10 to 14% in women’s average pay was reported in leather production and water transport, postal and courier activities, organisation of travels, sports activities, and events management, as well as several other sectors, manufacturing of coke and refined petrochemicals, cinema and television programme production, wastewater treatment, programme production and broadcasting, manufacturing of chemicals, extraction of oil and gas.

However, from the already listed sectors only in two of them (postal and courier services, oil and gas extraction) women’s average pay is higher than men’s amounting to EUR 1,856 (cf. men’s pay of EUR 1,552) and EUR 2,851 (cf. men’s pay of EUR 2,248), respectively; whereas in all the other sectors men earn more than women on average.

An average men’s pay is EUR 185 higher than women’s, but the gender gap has been narrowing

Despite the narrowing gender pay gap reported from April to July, in Lithuania men used to earn EUR 185 more than women: men’s average pay currently stands at EUR 1,596 against EUR 1,411 for women. Last April the gap reached EUR 190, with men’s average pay standing at EUR 1,581 against women’s EUR 1,391.

Aurimas Kačinskas, CEO of Creditinfo Lithuania, notes that in the absence of a more in-depth analysis, it is not feasible to assess gender pay gap; examination must be made into the types of positions held by men and women in order to identify the reasons behind differences in salaries.

“Publication of average pay is yet another indicator which can be used by future employees or partners to assess companies; knowledge of this information encourages a better understanding and awareness of the specificities of every company”, A. Kačinskas said.

The gap continues to grow in insurance, reinsurance, financial and telecommunication services, and pharmaceutical industry

Against the background of growing women’s average pay in most of the sectors, in 22 economic sectors the gender pay gap is widening. An average women’s pay dropped by 17.9% in insurance, reinsurance, and pension accumulation sector, where men earned EUR 3,179 per month on average compared to EUR 2,284 earned by women. A gender pay gap widened further from 11.1 to 11.5% in research and technical activities, pharmaceutical industry, power and gas supply, and air conditioning.

Gender pay gap continues to enlarge in the beverages’ industry, immovable property, construction of buildings, telecommunications, and financial sectors.

For instance, in telecommunications an average monthly women’s pay in July stood at EUR 1,602 compared against EUR 2,154 for men, in the financial sector these figures were EUR 2,433 and EUR 3,620, respectively.

The yawning gender pay gap is reported in air transport, where men earn EUR 3,932 per month on average, compared with women’s average monthly pay of EUR 2,385. Human resource management experts put this gap down to a higher number of men engaged in the aviation sector in better paid positions of pilots, whereas women work as flight attendants.

Meanwhile, it is worth mentioning that over three months the number of economic sectors with women earning more than men grew from 9 to 11. The sectors of education, libraries, land transport and transport via pipelines, social work, care services, furniture production, postal and courier services, tobacco and metal production were recently joined by fisheries and aquaculture companies, and motor vehicle manufacturing.

Earlier last June it was reported that, as of last April, out of 81 economic sectors in as many as 72 men receive higher pay than women.

For more information please contact:

Aurimas Kačinskas, CEO of Creditinfo Lithuania, (aurimas.kacinskas@creditinfo.lt; +37061810110).

Lithuanian corporate immunisation level is as high as 90% while others are below 30%

The share of immunised staff in different commercial companies may vary several times, the survey by Creditinfo Lithuania suggests. According to Statistics Lithuania (SL), the least immunised retailers (from 36.9 to 52%) work at markets and kiosks. The largest proportion of immunised staff after vaccination (up to 74.7%) has been reported in pharmacies, optics and supermarkets. Among all the sectors, the least active are construction and transport companies, but this indicator may well be explained by a large share of foreign nationals on their staff list.

According to SL data, in terms of the share of immunised staff in the commercial sector, companies selling bread, buns and confectionaries in specialty bakery shops take the last place, with slightly over one third (36.9%) of immunised staff. In other commercial segments, the percentage of fully immunised staff is within the range of 52–64%, with 60–87.2% of staff having received at least one vaccination doze.

Jekaterina Rojaka, Head of Business Development and Strategy at Creditinfo Lithuania, says that after the Statistics Lithuania launched publication of immunisation indicators on a company level, Creditinfo followed suit and started reflecting them in its information systems, while a growing number of users look for information on immunisation of potential business partners.

More staff got infected and recovered from the virus where the vaccination pace is slow

It appears from the publicly available data that in companies with staff delaying vaccination the proportion of staff infected or having recovered from the virus is higher. Obviously, the analysis of recovery indicators among staff suggests that many of these people (up to 12%) are among market and kiosk retailers. Within the category, the sub-category of textile, clothing and footwear retailers stands out where the full immunity (two vaccine dozes) within this group has been acquired by 52% of staff, another 12% of staff became immune after getting infected and recovering from the virus, bringing the overall immunisation level to 64%.

In comparison to workers in supermarkets, pharmacies and optics with 75% of fully vaccinated staff, the immunity after getting infected with the virus was reported from 1 to 5% of the labour force.

The largest number of immunised staff work for the financial services sector, the smallest number – in transport companies

The analysis of companies from other economic sectors suggests that among companies with 70–100% of immunisation level, those engaged in financial activities and services take the lead with 87.1% of immunised staff. Companies at the bottom of this group are from construction (38.7%) and transport sectors (30.3%). According to J. Rojaka, a low level of vaccination there may be explained by a relatively high number of foreign staff working in these sectors, leaving their immunisation indicators outside the scope of the national statistics.

Compared to other economic sectors, extractive industry and agricultural companies are moving at the slowest pace towards the set immunisation target of 70–100%, accounting for 46.6 and 47.8% of immunised staff, respectively.

In restaurants and hotels, which had been very actively promoting vaccination among their staff, at the end of August the immunisation indicator approached to 71.5 and 71.6%, respectively. J. Rojaka notes that these two sectors have achieved the major quality progress in terms of staff vaccination pace, reporting an increase of 45 percentage points in the number of staff vaccinated in August.

For more information:

Jekaterina Rojaka,

Head of Business Development and Strategy, Creditinfo Lithuania

Email: jekaterina.rojaka@creditinfo.lt;

Tel: +370 612 73515

Analysis of the Lithuanian construction sector

Financial and performance indicators in the construction sector reveal positive rather than negative trends. The boom in real estate emerging in the time of the pandemic has remarkably boosted the sectoral activity (during the first 6 months of this year alone the volume of constructions works grew by almost one fifth) and positively reflected in performance indicators of most of the companies. Sectoral earnings have been rapidly growing both on the domestic and foreign markets. After discounting the impact of seasonality and working days abroad, the volume of construction works is an increase of 21.5% year-on-year. The number of construction companies have been mushrooming, accounting for an increase by a third during the second quarter of this year compared to the previous year.

Financial statements filed by construction companies show that the number of construction companies in Lithuania in 2021 has grown by additional 531 from 15,784 to 16,316 (an increase of 3.4%) year-on-year. A very similar pace of growth (4.1%) was observed in the average corporate earnings (from EUR 809,994 to EUR 842,872). In terms of the staffing level, though, it has decreased slightly from 102,072 to 101,833. Despite a favorable situation, managers of construction companies are very cautious about the growth in the number of staff due to higher labour and other construction costs. Due to a more pessimistic mood in the sector, during summer this indicator started to decrease.

Another important positive factor is the decreasing number of debts and their aggregate values. For instance, during pre-pandemic August 2019 the number of corporate debts in construction industry stood at 12,336, with their aggregate value of EUR 128.7 mln. At the same period in 2020 the number of corporate debts stood at 11,539 compared against a reduced value of debt of EUR 94.3 mln. Although at the end of last August the number of corporate debts in the construction industry grew once again to 12,055, the aggregate debt value accounts for EUR 96.6 mln.

Some positive trends may be seen in the solvency of the construction industry. For instance, a year ago 23% of companies in this sector belonged to the high or highest group of bankruptcy risk, whereas this year the number of such companies dropped to 20%. In terms of delayed payments, some improvement may be observed too: last year the number of companies within the group of high and highest risk of delayed payments accounted for 47%, compared against 37% this year.

A number of construction companies going bankrupt has been decreasing steadily. In 2017-2020 the number of bankruptcies dropped from 366 to 163, whereas the updated statistics for this year give a solid ground to expect a further similar decrease in the number of reported bankruptcies.

Despite the reported drop in earnings in 2020 from 10% to 4% in comparison to 2019, other performance indicators in the construction industry have improved. For instance, the corporate sales median increased by 16% (from EUR 143,155 to EUR 166,133), the quick ratio has grown from 1.86 to 1.95, while the profit margin before tax increased from 1.25 to 1.35. The equity ratio has improved from 43.83 to 46.23, the accounts payable turnover decreased from 134 days to 128 days, whereas the accounts receivable turnover shortened from 57 to 51 day. EBITDA grew from 9.1 to 12.3%.

Jekaterina Rojaka,

Head of Business Development and Strategy, Creditinfo Lithuania

Creditinfo Lithuania included immunization levels into its list of corporate indicators

After the Department of Statistics launched publication of immunization levels in specific companies, credit office Creditinfo Lithuania immediately included this indicator into its corporate reports. From now on, clients ordering detailed information about a selected company will be able to see the proportion of immunized staff.

“The inclusion of immunization indicator into corporate reports will facilitate a better risk analysis of potential disruptions of activities due to staff illnesses which will help a business partner, or a client make further business decisions”, Aurimas Kačinskas, CEO of Creditinfo Lithuania said.

The first ever publication of immunization levels has demonstrated that, e.g., the largest share of immunized staff (80%) work for the IT sector, and the least immunized staff (as little as 27%) work for transportation companies. In comparison, as many as 80% of Creditinfo Lithuania staff have already been vaccinated.

Moreover, the official information published by the Department of Statistics will soon enable comparison of the share of immunized staff in one enterprise with counterpart organizations in the same business sector. To this end, an additional indicator is published as well – the so-called percentile. For instance, if an enterprise’s percentile is 100, it means that it is among one percent of companies with the highest immunization level. The lower the percentile, the fewer employees have immunity, i.e., have been vaccinated with at least one doze or have recovered from the coronavirus.

According to the Department of Statistics, for the purpose of confidentiality the percentage of immunization is indicated only for those workplaces with over 10 members of staff.

“We believe that monitoring these indicators contributes to the national fight against the Covid-19 pandemic, encouraging companies to take a more proactive approach with regard to staff vaccination”, A. Kačinskas said adding that “we always try to include new indicators into our reports in a timely manner so that our clients could benefit from exhaustive information about other companies”.

As of last May, Creditinfo Lithuania included into the list of monitored indicators information about average gender pay, and soon is planning to introduce yet another one – the sustainability indicator.