Creditinfo Launches ESG Hub to Fast-track Baltic Companies’ Access to Reliable Sustainability Data

New one-stop-shop solution aggregates information from more than 20 external sources, helping banks and businesses boost their ESG strategies, manage risk, and streamline their supply-chain transparency.

Creditinfo unveiled ESG Hub, the Baltic region’s first pan-regional platform that gives lenders and businesses instant, standardised access to the environmental, social and governance (ESG) data they need to comply with regulations, assess counterparties and execute sustainability strategies.

Building on Creditinfo’s long track-record of turning complex business information into accessible actionable insight, ESG Hub consolidates data from 20-plus public and proprietary data sources from Estonia, Latvia and Lithuania into one standardised API feed and ready-to-use report. By merging country-specific registries into a single, harmonised view, the platform lets banks and businesses manage ESG data uniformly across all three markets. Users can pull company-level metrics—from carbon emissions and energy intensity to board diversity and community impact—within seconds, eliminating the need to piece together separate national datasets manually.

“We want to accelerate the sustainability journey for the Baltic economies, and it all starts with easy access to trusted information. Until now, assembling ESG data has been difficult and time-consuming; companies have spent substantial time on these tasks, and the process has been inefficient,” said Elari Tammenurm, Regional Director, Continental Europe at Creditinfo. “With ESG Hub, any financial institution or company can integrate harmonised data directly into their existing workflows, cutting cost and complexity while improving decision speed.”

Proven model, now scaled to the Baltics

Creditinfo first introduced an ESG data service in Iceland in 2023; rapid adoption by local banks and corporates highlighted the growing importance of reliable sustainability intelligence. “The strong uptake we saw in Iceland showed us how big the need is,” noted Reynir Smári Atlason, Managing Director of Sustainability at Creditinfo. “We’re now bringing those learnings, and a richer dataset, to the Baltic markets.”

The company will continue to expand ESG Hub’s data source coverage and analytical modules over the coming months. Future roll-outs in additional Creditinfo markets are also planned.

For more information visit ESG Hub

Creditinfo Lithuania Analysis: In 2024, An Average of Three Companies Filed For Bankruptcy Daily

According to Creditinfo Lithuania’s analysis, 1,079 company bankruptcies were registered in Lithuania in 2024—a 16.1% increase compared to 929 cases in 2023. However, this figure is slightly lower than in 2022 when 1,087 bankruptcies were recorded (a 0.7% decrease).

Key Sectors Affected: Construction, Trade, Transport, and Manufacturing

Construction Sector Challenges

The construction sector faced the highest number of bankruptcies in 2024, with 243 cases, marking a 16.8% increase from 208 cases in 2023. However, this was a slight 2.5% decrease compared to 2022 (237 bankruptcies). Currently, 11,299 companies operate in the construction sector in Lithuania.

Dovilė Krikščiukaitė, Head of Legal at Creditinfo Lithuania, noted that the sector struggled with insufficient demand, particularly in real estate. However, engineering construction projects increased by 10.3%, and many companies remain optimistic, planning to hire more employees and anticipating growth.

Despite these challenges, economic analyst Aleksandras Izgorodinas from Citadele Bank projects fewer bankruptcies in 2025 due to declining interest rates in the eurozone. Improved real estate transactions and mortgage volumes are already evident, which could stabilize the construction sector further.

“However, I believe that in 2025, the number of bankruptcies in the construction sector will decline. With falling base interest rates in the eurozone, we are already observing a recovery in real estate transactions and mortgage volumes. Buyers are returning to the real estate market, and the cost of borrowing continues to decrease. This will lead to fewer bankruptcies in the construction sector in 2025. It is projected that the ECB will lower interest rates at least three more times this year, further supporting recovery in Lithuania’s construction and real estate sectors and reducing bankruptcy numbers,” said A. Izgorodinas.

Wholesale and Retail Trade

The wholesale and retail trade sector had the second-highest number of bankruptcies, with 237 cases, a 3.9% increase from 2023 (228 bankruptcies). However, this figure was lower than in 2022 (251 cases). With 23,601 companies, this sector remains the largest in Lithuania.

“Companies in this sector faced fluctuating demand, but recovering domestic consumption and increasing real wages resulted in higher revenues compared to the previous year,” explained D. Krikščiukaitė.

Transport Sector Under Pressure

The transport and logistics sector, comprising 8,684 companies, saw 134 bankruptcies—a dramatic 74% increase from 77 in 2023 and a 35.4% rise compared to 99 cases in 2022.

“Unlike the construction sector, where we see the first signs of recovery, the transport sector is yet to show improvement. For instance, Germany’s truck mileage index, which strongly correlates with Lithuania’s transport services export indicators, fell to its lowest level since the end of 2020 by the end of 2025, being 2% lower than at the end of 2024. This indicates that the transport sector will likely remain under pressure in the near future. The sector is highly sensitive to fuel price fluctuations and supply chain disruptions, which often create difficulties for smaller companies,” commented Citadele Bank’s economist.

Manufacturing Sector Struggles

The manufacturing sector, with 8,440 companies, recorded 121 bankruptcies in 2024—a 31.5% increase from 92 in 2023 and a nearly 25% rise compared to 97 in 2022.

According to Creditinfo Lithuania’s head of legal, reduced demand in European export markets, rising raw material costs, and higher energy expenses led to financial difficulties for many manufacturing companies.

Positive Developments in the Accommodation, Food Services, and Real Estate Sectors

Despite the rise in bankruptcies in the sectors, certain industries exhibited positive trends. In 2024, the number of bankruptcies in the accommodation and food services sector dropped by 20% to 66 cases compared to 82 cases in 2023. Moreover, this figure represents a 52% reduction compared to 2022, which saw 137 bankruptcies. Currently, 3,837 companies operate in this sector in Lithuania.

Similarly, the real estate (RE) operations sector, encompassing 6,621 companies, also demonstrated improvement. Bankruptcies in this sector decreased by 22.7% in 2024, from 44 cases in 2023 to 34 cases. In 2022, 33 insolvency cases were recorded in this sector.

Analysis of insolvent companies revealed that the total turnover of bankrupt companies in 2023 was €194.28 million, with the average annual turnover per company standing at €848,000. Notably, the workforce within these companies experienced a significant decline. At the beginning of 2023, these firms employed 7,292 workers; by October, this number had fallen to 5,551 employees.

“Monitoring the key operational metrics of business partners can help identify early warning signs. A decrease in workforce, reduction in the transport fleet, changes in management or shareholders, relocation of headquarters, or declining turnover are indicators that warrant close attention to ensure reliable partnerships and the fulfillment of financial commitments,” stated Dovilė Krikščiukaitė, Head of the Legal Department at Creditinfo Lietuva.

The head of Creditinfo Lietuva’s Legal Department also observed a trend toward younger companies becoming insolvent. In 2024, the average age of bankrupt companies was 10.58 years, compared to 11.68 years in 2023 and 12.31 years in 2022.

“This shift indicates that an increasing number of young companies are struggling to overcome market challenges and adapt to changing economic conditions. Young businesses often face financial management deficiencies, high costs, and intense competition, which exacerbate their difficulties,” added the Creditinfo Lietuva representative.

Lithuanian Paper Industry: Revenue Growth, Debt Increase & Decreasing Risk

Challenges from a Few Companies Distort the Overall Picture

An analysis by Creditinfo Lietuva reveals a controversial situation in Lithuania’s paper manufacturing sector. While the number of companies has decreased in recent years, the number of employees has grown. In 2023, sector revenues reached €829 million—a 51% increase compared to the beginning of 2021. However, there are worrying signs: the sector’s debt portfolio has grown nearly fivefold over four years. This negative trend is primarily driven by the difficulties of a few companies, while the sector itself demonstrates resilience. No bankruptcies have been recorded in the past three years, and the risk levels are nearly twice as low as the national business risk average.

Current State of the Sector

According to Creditinfo Lietuva, there are currently 176 companies operating in the Lithuanian paper manufacturing sector, employing 5,462 people. While the number of companies has gradually decreased from 191 in 2021 to 176 in November 2024, employee numbers have grown steadily, from 5,022 in January 2021 to 5,462 in November 2024.

Economic Indicators: Positive and Negative Trends In 2023, total sector revenues reached €829 million—4.6% less than at the start of the year (€869 million), but 21% higher than in 2022 (€684.6 million) and 51% higher than in 2021 (€548 million). Over a four-year period, average annual revenues per company increased from €4.2 million to €6.1 million.

The paper manufacturing sector includes companies producing pulp, paper, and cardboard, as well as corrugated paper and cardboard packaging, hygiene and household products, stationery, copy paper, envelopes, wallpapers, and other specialized products.

Debt Portfolio Increased

Fivefold At first glance, the sector has seen a significant increase in overdue financial obligations. Between 2021 and the end of 2024, the debt portfolio grew nearly fivefold, from €157.7K to €776.6K, while the number of debts increased only slightly, from 87 to 89 cases.

“A deeper analysis shows that the overall figures are skewed by issues faced by a few companies—one undergoing restructuring and another involved in legal proceedings. Excluding these, the sector remains stable, with the average debt amount per case decreasing from €2,999 in early 2024 to €2,803,” says Dovilė Krikščiukaitė, Head of Legal at Creditinfo Lietuva.

Bankruptcy Trends

From 2003 to the end of 2024, the paper manufacturing sector recorded 30 bankruptcies. However, insolvency cases have varied across periods. For instance, no bankruptcies occurred between 2022 and 2024 or from 2014 to 2015, while 2009–2010 saw 5 and 4 bankruptcies, respectively.

Risk Levels: Lower Than Other Sectors

Analyzing risk trends between 2022 and 2024, the paper manufacturing sector shows positive stabilization. Currently, 8% of companies are classified as high-risk for late

payments, and 5% are at high risk of bankruptcy. This means over 90% of companies are considered low- or medium-risk. In comparison, the national average bankruptcy risk is 9%, with 16% of companies at risk of payment delays.

“Aside from a few exceptions, Lithuanian paper manufacturers are relatively low risk. Compared to other sectors, this positions them as a stable part of the economy,” adds Krikščiukaitė.

Top Companies by Revenue and Employment

The top 10 Lithuanian paper manufacturers by revenue in 2023 are:

1. Nemuno banga (€178.2M)

2. Aurika (€70.3M)

3. DS Smith Packaging Lithuania (€59.4M)

4. Grigeo Klaipėda (€45.8M)

5. Grigeo Packaging (€36.4M)

6. Rietuva (€32.99M)

7. Pakmarkas (€27.1M)

8. Bigso (€24.9M)

9. Miko ir Tado leidykla (€24.3M)

10. Klaipėdos kartono tara (€23.8M)

Top employers in the sector include:

1. Nemuno banga (580 employees)

2. Aurika (481 employees)

3. Bigso (324 employees)

4. Grigeo Tissue (244 employees)

5. DS Smith Packaging Lithuania (214 employees)

Construction sector in Lithuania twice as risky as other businesses

Despite rising incomes and headcount, seizures amount to almost EUR 110 million

19% of construction companies are in the high and top bankruptcy classes and 31% are at risk of late payment, according to a recent study by Creditinfo Lithuania. Despite the number of employees and the rapid growth in revenues, the sector has already recorded 169 company bankruptcies this year. Nearly 11,000 debts have been registered, totaling more than €91 million. 1049 companies are subject to asset seizures amounting to almost €110 million.

There are currently 19850 construction companies registered in Lithuania, employing a total of almost 110 000 workers. At the beginning of this year, the number of companies in the sector was 20367, creating 108.2 thousand workplaces, while in 2023 the figures were 19167 and 107.7 thousand respectively.

According to data provided to the Centre of Registers, in 2023, construction companies in Lithuania together generated revenues of more than EUR 10.6 billion, representing 14.7% of the country’s GDP. In comparison, in 2022, construction companies’ gross revenues were 22.6% lower at EUR 8.7 billion.

Following the data provided by the companies, the top ten construction companies in terms of revenue in 2023 are Kauno Tiltai (EUR 192.9 million), YIT Lietuva (EUR 191.1 million), Fegda (EUR 184.2 million), Conres LT (EUR 117.3 million), Infes (EUR 107.3 million), Green Genius (EUR 102.7 million), “Merko statyba (EUR 97.8 million), Žilinskis & Co (EUR 94.4 million), Autokausta (EUR 94.3 million), Stiemo (EUR 87.4 million).

Despite the year-on-year increase in revenues, the construction sector is twice as risky as any other business in Lithuania. Currently, 19% of construction companies are in the high and highest bankruptcy classes, while almost one third (31%) are at risk of default. The sector has a similar risk profile from the beginning of 2023. Over the last 5 years, the highest risk levels were reached in 2020 and 2021, when a quarter of construction companies were close to bankruptcy and almost half of the companies (47%) were at risk of default.

In comparison, the average riskiness of all Lithuanian businesses is twice as low: 9% of companies are in the high and highest risk classes, while 16% are at risk of default.

Since 2007, 4,497 construction companies have gone bankrupt in Lithuania, with an average of 254 each year. The highest number of bankruptcies was recorded in 2009, when 445 companies became insolvent. This year, 169 construction companies went bankrupt between January and September.

The average amount of seized assets increased by 34.7% to EUR 105 thousand

Currently, 10892 debts of construction companies are registered in the credit bureau system, with a total amount of EUR 91 million and an average debt of EUR 8 360. Compared to the beginning of January 2024, the number of debts exceeded 13,000, the total amount was €164 million, and the average debt size was 1,5 times higher (€12,602).

According to the data of the Credit Bureau, there are currently 2209 seizures on construction companies, including 1043 seizures with monetary value, for a total amount of EUR 109.8 million. The number of construction companies with at least one attachment is 1049 and the average attachment per company exceeds EUR 105 000. At the beginning of this year, the number of seizures was 2,702, with 1,293 seized companies, and the average amount of a single seizure was EUR 68.7 thousand, 1/3 (34.7%) lower than at present.

“If you notice in the credit bureau’s systems that a business partner or client has seizures, please be careful. It is a serious sign that the company is at risk of defaulting on its payments,” advises Rasa Rasickaitė, Risk Assessment and Management Expert at Creditinfo Lithuania. Asset seizure is a compulsory restriction of the ownership right to property, which can be applied by state authorities to secure evidence, civil action, possible confiscation of property, as well as the collection of fines and unpaid payments, satisfaction of creditors’ claims, and fulfilment of other claims and liabilities. Therefore, when you see a registered seizure, you should also pay attention to other available information, such as court information, debts to creditors, the tax authorities and the social security system.”

According to Rasickaitė, in the event of a seizure of assets, it is advisable to find out the reason for which the seizure has been registered, what assets have been seized, and whether the seized assets are allowed to be disposed of in the course of the company’s business. If there are doubts about the ability of the business partner to pay, it is advisable to ask for prepayment or guarantees.

One in five construction companies on the brink of bankruptcy in Lithuania

As shown in a recent analysis of the construction sector conducted by Creditinfo Lietuva, almost a fifth (18%) of construction companies1 are currently on the brink of bankruptcy, while almost a third (31%) are at risk of defaulting on their payments. According to publicly available data2, construction companies, as a whole, exhibit shorter operating histories and offer lower wages compared to other sectors. Financial experts are therefore advising caution when engaging with construction firms.

There are currently 19,167 construction companies in Lithuania, employing almost 108,000 people. The numbers of construction companies and their employees have shown consistent growth since 2020. In 2020, there were 16,144 construction companies with an employee count of nearly 102,000. By 2021, the numbers had risen to 17,171 companies and over 102,000 employees, and at the beginning of 2022, the sector boasted 18,512 companies, employing in excess of 106,000 people.

The average age of a construction company CEO is about 46 years, with a striking 87.5% of these leaders being male. Compared to other sectors, construction companies have a comparatively shorter average lifespan in the market, standing at 10 years, in contrast to the national average of over 13 years.

Despite witnessing among the fastest growth in the current year, salaries for construction workers still lag behind the Lithuanian average. According to data from Sodra, construction worker wages surged by 22% year-on-year in the second quarter, reaching EUR 1,300 before tax (EUR 880 net), while the average earnings of full-time workers across Lithuania rose by 12.3% year-on-year, amounting to EUR 1,980 before tax.

The risk of bankruptcy among construction companies is twice as high as the national average

Currently, 18% of construction firms fall into the high and highest bankruptcy risk categories, compared to 20% at the beginning of this year and 19% at the beginning of 2022. The high and highest risk classes of late payment now account for 31% of construction companies, up from 37% at the beginning of 2023 and 34% at the beginning of last year.

For all companies in Lithuania, excluding the construction sector, 9% of all companies in the country were in the high and highest bankruptcy risk classes at the beginning of 2023, compared to 12% at the beginning of 2022. At the beginning of this year, 17% of all Lithuanian companies belonged to the high and highest risk classes of late payment, with 21% at the beginning of 2022.

“Although the construction sector has experienced a period of growth in recent years, it is particularly sensitive to borrowing conditions, fluctuations in demand and geopolitical changes. During the pandemic, builders experienced a boom in demand – with many people deciding to improve their homes – low energy prices and relatively cheap borrowing. Subsequently, the construction sector encountered a number of challenges stemming from disrupted supply chains and the need to withdraw from cooperation with sanctioned countries,” explains Ekaterina Rojaka, Head of Business Strategy and Development at Creditinfo Lithuania. “In recent months, with the European Central Bank raising its base interest rates, borrowing has become a more costly affair, reducing people’s ability to borrow, and homes built with credit have been slower to sell.”

This year, bankruptcy proceedings were initiated for 136 construction companies

Since 2007, a total of 44,256 construction companies have been declared bankrupt in Lithuania. The highest number of bankruptcies occurred in 2009 (445), 2016 (351) and 2017 (367). Only in 2007 was the number of bankruptcies below 100, with a total of 67. In Lithuania, 163 construction companies faced insolvency in 2020, 131 in 2021 and 237 in 2022. In the first 8 months of this year alone, 136 construction companies in Lithuania have declared bankruptcy.

As of the beginning of September this year, there were 11,512 construction company debts on record, collectively burdened with nearly EUR 90 million in debts, with 962 new debts registered in the first 8 months of the year, according to the credit bureau systems. The average size of a single debt is EUR 7,800.

“When entering into contracts with construction companies, it is advisable to pay more attention to their risk assessment and to clearly negotiate payment terms,” Rojaka commented.

According to data provided to the Centre of Registers, the top 10 construction companies with the highest revenues last year are: YIT Lietuva (EUR 140.6 million), AB Kauno Tiltai (EUR 134.4 million), Conres LT (EUR 100.1 million), Autokausta (EUR 83.2 million), Tetas (EUR 79 million), Staticus (EUR 75.9 million), Merko Statyba (EUR 70.4 million), Žilinskis ir Co (EUR 68.7 million) and INGUS (EUR 63.9 million).

Almost one-fifth (19%) of companies in this sector have not yet submitted their financial statements for 2022.

According to Rojaka, state orders and building modernisation programmes will support the construction sector’s activity in the near future, as demand for real estate slows down. However, falling demand has only a limited impact on the final prices of construction services, as cheaper building materials do not compensate for the sector’s rapidly rising wages, which account for more than a quarter of total construction costs. As a result, construction continues to become more expensive, with a 3.7% year-on-year increase in construction costs in July, with the fastest increase in building repair costs, which rose by 9.2%.

More information:

Jekaterina Rojaka, Head of Business Strategy and Development at Creditinfo Lithuania (jekaterina.rojaka@creditinfo.com)

Or visit: lt.creditinfo.com/en

Notes:

1 In this report, construction companies are defined as companies that have publicly declared to the State Data Agency (SDA) the activity codes of Section F (41-43) of NACE2 as the company’s main activity.

2 The data in this press release is based on information publicly provided by the State Enterprise Centre of Registers, SODRA, the State Data Agency (VDA), and other sources.

Transport business in the Baltics is in recession, with only Lithuania experiencing a slightly brighter picture

Coface records recovery in air transport, but pre-pandemic figures not yet reached.

The transport sector is the one with the highest improvement in risk scores in the latest Coface Quarterly Survey, although the global macroeconomic outlook remains uncertain. Coface experts note that air transport forecasts and new aircraft orders are providing greater optimism. Transport business is rated higher in Western Europe, the Middle East and Japan, while in Central and Eastern Europe (CEE), including the Baltic states, the transport sector continues to be rated the highest risk. The transport sector in Estonia and Latvia is facing more challenges this year, while in Lithuania the situation has started to improve since Q2, with a decrease in bankruptcies and an increase in the forecasts for businesses.

According to Coface experts, the higher scores in the transport sector are mainly due to the recovery of the Chinese economy and global tourism, as well as to public policy decisions, such as the priority given to rail traffic in Germany. However, overall risks to the transport sector remain very high due to high energy costs and demand still below pre-pandemic levels.

Head of Coface Baltics, Mindaugas Sventickas, points out that it is air transport that has been the activity most affected in the global transport sector, and that it is now recovering rapidly. This is due to the gradual economic recovery from the second half of 2021 onwards, significantly influenced by the opening up of Japan (end of 2022) and China (early 2023), which has facilitated travel conditions for international tourists.

The Coface survey shows that while the number of commercial flights has increased and is now even above pre-pandemic levels, seat occupancy rates remain lower. For example, in the Asia-Pacific region, total passenger traffic in April 2023 increased by 171% compared to April last year, thanks in particular to China. Despite the strong growth, demand in this region remains lower than in 2019 (-18% in April 2023 compared to April 2019).

New orders for Airbus and Boeing aircraft are rising: aiming to fly greener and save fuel

In Western Europe and the United States, Airbus and Boeing have also reported an increase in aircraft orders, reaching 774 Boeing and 820 Airbus aircraft in 2022. At the 2022 Paris Air Show, a number of new orders were announced, with Air IndiGo ordering 500 A320 aircraft and Air India ordering 250 Airbus and 220 Boeing aircraft. According to the experts at Coface, this acceleration in the aerospace industry has prompted the decision to improve the risk assessment of the transport sector in some countries, e.g. France. Many of the production processes of Airbus are carried out in France, with production sites spread over Germany, Spain and the United Kingdom. This has contributed to a better assessment of the transport sector across Western Europe.

“It is also worth noting that the main players in the air transport industry are pursuing a strategy that takes environmental concerns into account. On the one hand, this motivates manufacturers to innovate in order to develop ‘cleaner’ aircraft. On the other hand, it encourages airlines to upgrade their fleets to use less energy,” comments Sventickas.

Cargo transport by sea decreases by almost one third

The situation is different in maritime transport, where activity is slowing down slightly after two exceptional years. Declining sea freight rates, high energy costs and stagflation are adversely affecting the financial performance of sea carriers. The revenues of Maersk and CMA CGM in Q1 2023 decreased by 26% and 30% respectively compared to Q1 last year, although they remain significantly higher than in Q1 2019.

This drop in revenue is primarily due to price effects (a fall in freight rates), while the drop in volumes is smaller, with a 3% annual decrease in the container index for January–April 2023. This drop in volumes is partly passed on to rail and motor transport, which is primarily used for the transport of cargo from ports.

Passenger transport in the Baltic States has not yet reached pre-pandemic levels

When analysing air passenger flows in the Baltic states for the period 2019–2023, the highest passenger traffic is traditionally observed in Q3 of each year. After the pandemic, air passenger traffic in all of the Baltic states, although slowly increasing, has not yet reached the levels recorded in 2019. For example, in Q3 2019, the number of air passengers in Estonia reached 954,000, in Latvia 2,299,000 and in Lithuania 1,821,000. In the same period last year (Q3 2022), the figures were 841,000 (88%), 1,711,000 (71%) and 1,677,000 (92%) respectively. According to Eurostat and Coface, the total number of passengers carried by air in the Baltic states in 2022 was 13,434, compared to 6,094 in 2021, 4,657 in 2020 and 17,548 in 2019.

The situation in rail passenger transport is slightly better. For example, in Q3 2019, the number of passengers in Estonia was 2,105,000, in Latvia 5,256,000 and in Lithuania 1,287,000. In the same period last year, the figures were 1,837,000 (87%), 4,835,000 (92%) and 1,292,000 (100%) respectively. The total number of passengers carried by rail in the Baltic states in 2022 was 27,289, compared to 21,069 in 2021, 22,085 in 2020 and 31,986 in 2019. In Q1 of this year, the figure for the Baltic countries was 6,485.

Sventickas notes that the Lithuanian transport sector is distinguished from other Baltic countries by more optimistic forecasts for 2023: “Although the situation in the Lithuanian transport sector deteriorated in the first quarter of this year, we have seen some positive trends since the second quarter of this year: the transport of freight by sea and water has stabilised and the transport of freight by land has returned to almost pre-pandemic levels. Since February this year, the forecasts of transport companies in Lithuania have become more stable, while previously they had been declining for several months.”

Creditinfo: Optimism of Lithuanian transport companies is good news for almost 200,000 employees in the sector

According to 2022 data, Lithuania’s transport and storage sector generated 11.2% of the country’s GDP, which is 2.6 times more than the average for other EU countries. In total, there are currently 8,568 transport and logistics companies in Lithuania, employing 171,300 people, i.e. a quarter more than in 2019.

Jekaterina Rojaka, Head of Business Development and Strategy at Creditinfo Lietuva, points out that the majority (72%) of companies in the transport sector in Lithuania are involved in road freight transport. According to the data of July this year, even 6,195 out of 8,568 transport companies registered in Lithuania indicate that their main activity is transportation of goods by land. Transport accounts for over 55% of Lithuania’s total exports of services. The number of air and water transport companies is 21 and 37 respectively; 2,233 companies in the sector provide storage and transport-related activities and 82 companies provide postal and courier services.

“During the pandemic, the risk exposure of Lithuanian transport companies increased due to travel restrictions, changes in the demand for goods, and then the rise in fuel prices,” says Rojaka. “In 2022, there was a sharp increase in the number of bankruptcies in the transport sector, which started to stabilise this year. In the first half of this year, bankruptcies in the transport sector accounted for only 6% of all company bankruptcies, compared to 24% in the trade sector and 20% in the construction sector. In total, 35 transport service companies have gone bankrupt since the beginning of the year, compared to 50 companies in the sector that went into bankruptcy in the same period last year.”

Rojaka says that although the number of bankruptcies of transport companies has decreased, the number of new companies has slowed down slightly: last year, despite bankruptcies, new companies were actively registering, while in the first four months of this year that number has contracted by 2%. According to a representative of the credit bureau, transport companies have started to borrow more, and the average debt of a company has increased by approximately 35%. There is also a lower number of companies with a low risk of bankruptcy, that is 58.1%, compared to the overall assessment of Lithuanian business of 69.5%. The share of companies in the transport sector experiencing financial difficulties in 2022 is lower than the national average, and amounts to 13.2% (compared to 17.6% for the economy as a whole).

“With the slowdown in domestic consumption in the EU, transport service providers continue to face challenges this year, with competition in the sector increasing due to limited demand, and service fees shrinking. Waterborne transport has seen a particularly sharp fall: The Baltic Dry index contracted by 57% over the year, and this year similar trends have been observed in road transport,” explains Rojaka. “The best short-term prospects for the sector at the moment are for airlines, which are steadily both increasing the number of flights and trying to rebuild the revenues lost in the pandemic. With inflation gradually slowing and demand stabilising, the situation for land and water transport companies should improve next year.”

Creditinfo Lithuania.

Visit: www.lt.creditinfo.com

Webinar: Baltic Market Overview

Register and join Jekaterina Rojaka, COO Creditinfo Lietuva , as she hosts another session on the Baltic market overview.

During this session, you will get the latest updates on the following:

- Improving sentiments – will it strengthen economic growth?

- Rising interest rates – what is the impact on the market?

- Sectoral perspective – losers and winners

Please complete the registration form below to receive the event link. The session will be in English – http://ow.ly/MSjh50NHVVX

Lithuanian debts increased by €6.8 million since the beginning of 2023

According to Creditinfo Lithuania’s latest analysis, Lithuanian debts have increased by €6.8 million since the beginning of the year, reaching a total of €364.8 million.

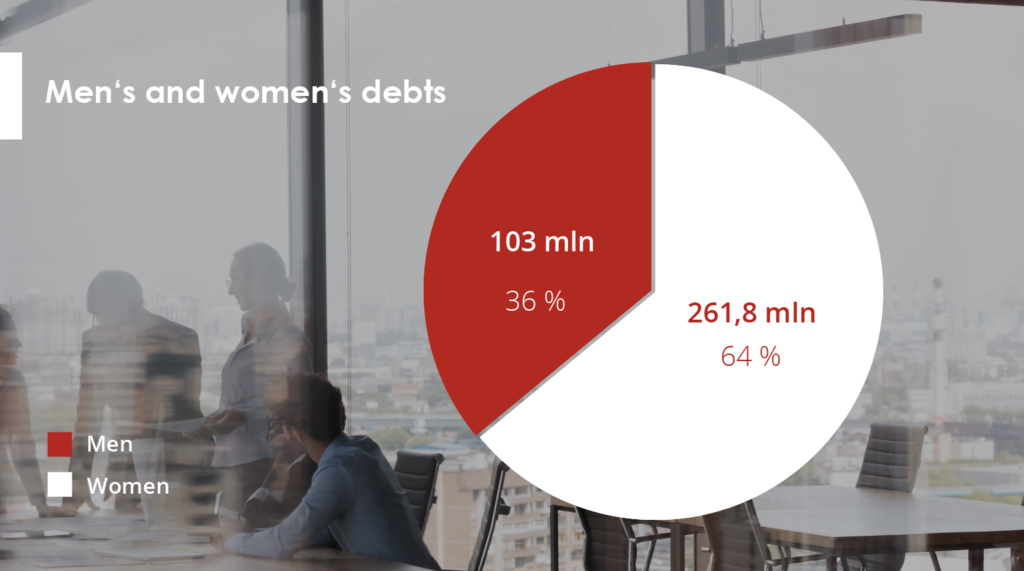

Of this amount, male’s debts stand at €261.8 million, while female’s debts are at €103 million. This is almost €6.8 million more than at the beginning of this year (€358 million). The total number of borrowers has also risen by 5,000 in the first quarter of this year, with the current total standing at almost 201,000.

Creditinfo Lithuania has recorded almost 201,000 debtors in its systems for March, with a total of 235,300 individuals having 235,300 debts in Lithuania.

After a more detailed examination of the debtor data, it was found that over 129,000 males and 72,000 females are currently in debt, making up 64% and 36% of all debtors respectively. Additionally, 32,500 males and almost 20,000 females have multiple debts, with 25.3% of male debtors and 27.7% of female debtors holding two or more debts.

On average, males owe €2,029, which is 30% more than the average debt owed by females (€1,435). This trend, coupled with the higher number of male debtors, results in men holding 78% of the total debt amount, while women hold only 22%.

During the first quarter, an additional 5,000 individuals in Lithuania fell into debt.

In March, the total number of individuals in debt amounted to 201,000, marking an increase of 5,000 from January’s 196,000. The total value of debt owed by all debtors also rose from €358 million to €364.8 million, with the total number of debts recorded in the credit bureau system increasing by 5,300. The largest number of new debts to households registered in the first quarter of this year, after debts to the financial sector, were for utilities and energy, with a total of 1,518 debts (12%).

“The analysis suggests that the majority of new debts recorded this year can be attributed to the energy and heat price crisis. Rising fuel costs have resulted in increased indebtedness, with people seeking short-term financing in order to balance consumption and expenses,” explains Aurimas Kačinskas, the Head of Creditinfo Lithuania. “Not everyone has had sufficient time to alter their financial habits, which has resulted in the growing number and value of debts.”

Men aged between 35 and 45 are considered to be the most high-risk debtors

Despite fluctuations in the number of borrowers and their levels of indebtedness, the typical borrower profile has remained consistent in recent years. Men aged 35-45 are the riskiest debtors, with debts amounting to €75 million, accounting for almost 29% of the total amount owed by men. The second riskiest group is men aged 45-55, with €61 million in debt, representing 23.3% of the total amount owed by men. In third place are men aged 25-35, who hold €55 million in debt, accounting for 21% of the total amount owed by men. Men aged 55-65 hold €43 million in debt, while those over 65 hold €17 million. Men under 25 hold the lowest amount of debt at almost €15 million.

Among female debtors, the under-25 age group has the lowest amount of debt, while other age groups have the following distribution: €29 million (45-55), €26 million (35-45), €20 million (55-65), and €17 million each (25-35 and over 65).

According to Mr Kačinskas, it is important for citizens to assume their financial obligations responsibly and meet them on time to maintain a positive credit history, which determines their access to financial services, loans, credit cards and payment provisions.

One of the safest businesses in Lithuania – Dental Services

The profitability of some companies is almost half their revenues, very few go bankrupt.

Vilnius, Lithuania 06/02/2023. Although most dental businesses are small and usually employ fewer than 10 people, this is one of the most stable businesses in Lithuania. Profitability often exceeds one-third of income and only a few become insolvent. Dental businesses are 7 times less likely to go bankrupt than the average insolvency across all other businesses, according to an analysis conducted by Creditinfo Lithuania.

According to data from January 2023, there are currently almost 2,000 dental businesses in Lithuania employing 9,500 people. The number of companies and their employees is growing year on year. Dental businesses are generally small, with more than half of them employing fewer than 10 people. Only 12 organisations have created more than 50 jobs, while the largest dental service companies are Vilnius University Hospital (293), SB Dental Clinic (168), Denticija (153), Smile Academy (126), Smile Laboratory (124), Vilnius Implantology Centre Clinic (93), Panevėžys City Dental Clinic (72), Laudenta (71), Pasirink (66) and Žvėrynas Dental Clinic (59).

Revenues grow year on year, profitability remains high

Despite the pandemic’s restrictions on the medical services sector between 2020 and 2021, the total revenue of dental companies has grown consistently year on year, reaching €294.6 million in 2021, an increase of 39.8% compared to 2020 (€210.7 million), which in turn is an increase of 76% compared to 2019 (€167 million).

The top 10 companies with the most revenue in 2021 are SB Dental Clinic (€8.2 million), Vilnius Implantology Centre Clinic (~€7 million), Denticija (€3.2 million), Smile Academy (€3.1 million), Prodenta (€3.1 million), Žvėrynas Dental Clinic (€3 million), Sveikatos Gija (€2.9 million), Šiauliai Implantology Centre (€2.8 million), Laudenta (€2.6 million) and Dental Harmony (€2.6 million).

Dental service companies are characterised by relatively high profitability, reaching up to 45%. The top ten companies with the highest profits in 2021 are Laudenta (€922 thousand), SB Dental Clinic (€917 thousand), Implantera (€739 thousand), Šiauliai Implantology Centre (€713 thousand), Smile Design (€688 thousand), Vilnius Implantology Centre Clinic (€644 thousand), Klaipėda Orthodontics Centre (€592 thousand), Dantima (€556 thousand), Donatas Jurgaicis Odontology Clinic (€529 thousand) and Teeth Centre (€512 thousand).

“The dental services business has advantages – patients usually pay for services immediately, which speeds up the turnover of funds. In addition, some dental services are subject to significant VAT exemptions, which reduces the tax burden and increases the profitability of the companies,” says Jekaterina Rojaka, Head of Business Development and Strategy at Creditinfo Lithuania.

However, not all companies were profitable, with 148 dental service providers declaring a loss in 2021, compared to 128 in pandemic year 2020 and 133 in pre-pandemic year 2019.

Dentists 7 times less likely to go bankrupt

The dental services sector has a particularly low risk of bankruptcy compared to all other sectors, with 1% of firms currently at high risk of bankruptcy and 0% at the highest risk. The high and highest risk classes for late payment are 3% and 2% of companies, respectively. The riskiness of dental firms was slightly higher at the beginning of 2021, with 4% of firms in the high bankruptcy risk class (none in the highest) and 11% in the high and highest delayed payment risk classes.

No dental companies went bankrupt in 2021 or 2022, while 26 firms have become insolvent since 2003, an average of 1-2 per year.

The dental business is characterised by a low level of debt. As of January 2023, there were 98 registered debts in the credit bureau’s system, totalling €95 thousand. The average debt was €971.

Compared to companies operating in other sectors in Lithuania, dental service companies are 7 times less risky. For example, in January this year, 1.3% of dental businesses were classified as high and highest risk, compared to an average of 9.5% for all other businesses in Lithuania. In terms of the risk of late payment, 4.5% of firms were in the high and highest risk classes, while the average for all other firms was 17.2%.

Almost a fifth of dental businesses (359) have not yet submitted their financial statements for 2021.

More information:

Jekaterina Rojaka, Head of Business Development and Strategy, Creditinfo Lithuania (jekaterina.rojaka@creditinfo.com)

Travel agencies in Lithuania are slowly rising from the ashes

Revenues doubled in a year but remained three times lower than before the pandemic.

Vilnius, Lithuania, 24/01/2023. Travel agencies in Lithuania that declared their income in 2021 earned almost twice as much as in the previous year. However, compared to income in 2019, they earned almost three times less, according to an analysis carried out by the credit bureau Creditinfo Lietuva. Almost 100 tourism companies were loss-making. With the increase in travel flows, the number of debts increases and their average size grows.

There are currently 783 companies in Lithuania for which tour organisation is the main activity. In 2021, travel agencies declaring revenues collectively earned more than €171 million, almost double (82%) the pandemic year 2020 (~€94 million). However, travel agencies are still a long way from a real recovery – for example, in 2019, their revenues were almost €474 million, but fell more than fivefold in the aftermath of the pandemic.

According to 2021 data, the largest annual revenue was earned by the following companies: Novaturas (€108,995 million), Tez Tour (~€60 million), Itaka Lietuva (€12.5 million), Coral Travel Lithuania (€9.5 million), Kidy Tour (€8.9 million), Estravel Vilnius (€6.3 million), Estekspress (€4 million), Traveldeals LT (€4 million), Glotera (€3.6 million) and ZIP Travel (€2.9 million).

The top ten most profitable travel agencies are Novaturas (€909 thousand), Baltic Tours Group (€633 thousand), Vestekspress (€530 thousand), Glotera (€336 thousand), Traveldeals LT (€307 thousand), Baltic Clipper (€288 thousand), Baltic Travel Service (€271 thousand), TEZ Tour (€215 thousand), Estravel Vilnius (€158 thousand), Riviera Tours (€148 thousand) and ZIP Travel (€123 thousand).

Staff numbers shrink by a quarter

In total, travel agencies currently employ almost 2,000 employees (1,850). While the number of enterprises has remained almost constant over the past few years (776 in 2019, 787 in 2021), the number of employees has fallen by almost a quarter since 2019, from 2,426 to 1,850.

Travel agencies are more often headed by women, accounting for almost 56% of all managers. The average age of a travel agency manager is 49 years and the average age of a travel agency is over 15 years.

In the travel sector, men’s salaries are higher than women’s – as of November 2022, the average salary for men was €2,659 per month, while for women it was €2,014 per month. At the start of 2022, the average salary for women was €2,053 per month and for men was €2,364 per month.

State support has prevented more bankruptcies

Since 2004, a total of 94 travel agencies have gone bankrupt in Lithuania, with the highest number of bankruptcies recorded in 2009 (10) and in 2015 (12). In 2022, there were 5 travel agency bankruptcies, while there were 3 in 2021 and 4 in 2019. No travel agency bankruptcy was recorded in pandemic year 2020.

“The travel sector was one of the hardest hit by the pandemic, along with hotels and restaurants. During the pandemic, when revenues from tour operators dropped fivefold, it was state support that saved the sector from bankruptcy,” explains Aurimas Kačinskas. But the challenges of the pandemic were replaced last year by new challenges – the war in Ukraine and the sanctions imposed on Russia have exacerbated the energy crisis, fuel prices have risen and many travel routes have been disrupted. The slower-than-expected recovery of the air transport sector, with a sharp increase in fares, is having a negative impact on the business of tour operators, preventing them from recovering faster.

According to the head of the credit bureau, it was state support that determined the stability of the number of enterprises and the discipline of submitting financial statements – compared to other sectors, only 90 travel agencies did not submit their financial statements for 2021, making them ineligible for state support.

However, a risk analysis of travel agencies shows that there have been both positive and worrying signs in the recent period. For example, as of January this year, 9% of companies were in the high and highest classes of bankruptcy, compared with 12% a year ago. In terms of delayed payments, 17% of companies are currently in the high and highest risk classes, down from 21% last year.

Compared to 2020 and 2021, the recent increase in debt is slightly higher and the average amount of debt per person is growing. At present, 306 debts have been registered in the credit bureau system, amounting to more than €349 thousand, with an average debt of €1,141. A year ago, the number of debts was 316, amounting to €351 thousand, with an average debt of €1,112. In January 2020, 255 debts amounting to €203 thousand were registered, with an average debt of €798. 335 travel agencies mostly owe money to Sodra (€3 million). The debt of 158 travel agencies to telecommunications companies amounts to €222 thousand. 8 travel agencies owe €74 thousand to financial companies.

“The tour operator business is recovering, but revenue growth is slower than expected in the wake of the pandemic due to the many geopolitical and economic shocks around the world. The tourism sector is currently encompassed by a number of risks, so it is advisable to keep a close eye on the changing financial indicators of partners organising the trips,” concludes the head of the credit bureau.

More information:

Aurimas Kačinskas, CEO of Creditinfo Lithuania (aurimas.kacinskas@creditinfo.com)