Creditinfo completes strategic acquisition of Ugandan and Namibian credit bureaus

Latest acquisitions cement credit expert’s position as leading solutions provider in Africa.

Kampala and Windhoek/London, 25th May 2023 – Creditinfo Group, the leading global service provider for credit information and risk management solutions, today announces the acquisition of two credit bureaus in Uganda and Namibia. As part of the acquisition, Creditinfo has taken on all employees working in the credit bureaus, which were previously owned by Experian. Creditinfo will combine their invaluable local expertise with its own extensive experience in delivering private credit solutions to African and European nations to help millions access finance.

Creditinfo has a unique mix of market knowledge that it will draw on to complement the work of the strong management teams already in place in Namibia and Uganda. Its experience working with more traditional lending markets in Europe combined with its knowledge of the different trends in lending markets in sub-Saharan Africa – such as the drive-in mobile wallet use in Kenya – will help both Namibia’s and Uganda’s credit bureaus go from strength to strength.

Coupling this experience with its advanced software and analytics products, Creditinfo will deliver its world-leading credit bureau solutions to help the two bureaus facilitate access to finance for both individuals, SMEs, and corporates in the regions, whatever their social and economic needs.

Paul Randall, CEO at Creditinfo said: “We are committed to sustainably growing our business and identifying ideal opportunities to add strong and profitable credit bureaus to the Creditinfo Group, while helping more local citizens and businesses access finance. Uganda and Namibia are ideal partners for us in this respect and all our new employees are a credit to the Creditinfo name. As the leading credit bureau provider in Africa, we eagerly look forward to working together to provide the best service possible in each country”.

Mark Charles Mwanje, Country Manager of Uganda said: “We are delighted to join the Creditinfo Group. We believe their years of expertise and knowledge will be a great asset to our existing team of dedicated and talented employees. We look forward to joining forces to help the local people and our growing economy.”

Karin Jansen van Vuuren, Country Manager of Namibia said: “Working with Creditinfo provides us the chance to tap into new opportunities for further growth. The company’s in-depth experience will be instrumental in helping banks and other lenders to extend credit, while ensuring we’re still a private credit bureau run by local people for local people, with all their best interests at heart.”

-ENDS-

About Creditinfo

Established in 1997 and headquartered in London, UK, Creditinfo is a provider of credit information and risk management solutions worldwide. As one of the fastest-growing companies in its field, Creditinfo facilitates access to finance, through intelligent information, software, and decision analytics solutions.

With more than 30 credit bureaus running today, Creditinfo has the most considerable global presence in this field of credit risk management. For decades it has provided business information, risk management and credit bureau solutions to some of the largest, lenders, governments, and central banks globally to increase financial inclusion and generate economic growth by allowing credit access for SMEs and individuals.

For more information, please visit www.creditinfo.com

Credit Bureaus and why they will remain important in the years to come

As the financial industry continues to evolve, credit bureaus need to continue to adapt. There are many compelling reasons why credit bureaus will continue to play a vital role in the future of lending and credit. In this blog, we’ll explore the benefits of credit bureaus and why they will remain important in the years to come.

1. Efficient and standardized credit data

Credit bureaus provide an efficient and standardized way to collect and store credit data. This allows lenders to quickly access the credit history and credit scores of potential borrowers, which is essential for making informed lending decisions. Without credit bureaus, lenders would need to spend more time and resources gathering credit data from various sources, which would slow down the lending process.

2. More accurate credit models

Credit bureaus are constantly refining their credit models to improve accuracy and predictiveness. By analysing large amounts of credit data, credit bureaus can develop more sophisticated credit models that consider a wide range of factors, such as payment histories, outstanding debts, and length of credit history. These models provide lenders with a more accurate picture of a borrower’s creditworthiness, helping to reduce the risk of defaults and delinquencies.

3. Increased access to credit

Credit bureaus play a critical role in expanding access to credit. By providing lenders with access to credit data, credit bureaus make it easier for individuals and businesses to obtain loans and credit cards. This is particularly important for people with limited credit histories or who have had past credit problems, as credit bureaus provide lenders with a way to evaluate these borrowers’ creditworthiness.

4. Protection against fraud and identity theft

Credit bureaus also play a key role in protecting consumers against fraud and identity theft. By monitoring credit reports for suspicious activity, credit bureaus can help detect and prevent fraudulent activity. Additionally, credit freezes and fraud alerts can be placed on credit reports to prevent unauthorized access to credit data.

5. Continued relevance in a changing industry

While the financial industry is evolving rapidly, credit bureaus will continue to be relevant in the future. As new technologies and data sources emerge, credit bureaus will adapt and incorporate these changes into their credit models. Additionally, credit bureaus will likely face increased competition from fintech startups and other companies, which will push them to innovate and improve their offerings.

In conclusion, credit bureaus are essential to the lending and credit industry. By providing lenders with access to credit data, credit bureaus make it easier for individuals and businesses to obtain loans and credit cards. Additionally, credit bureaus play a critical role in expanding access to credit, protecting consumers against fraud and identity theft, and adapting to a changing industry. As the financial industry continues to evolve, credit bureaus will remain a vital part of the lending and credit ecosystem.

Gary Brown,

Head of Commercial Development, Creditinfo Group.

AS Creditinfo Eesti appoints Elari Tammenurm as new CEO

Estonia, 9th May 2023 – Creditinfo Group, a global service provider for credit information and risk management solutions, today announces the appointment of Elari Tammenurm as the new Chief Executive Officer (CEO) of its Estonian branch. Elari will support and maintain Creditinfo’s legacy as a leading partner for business and risk management decision making and drive the sustainable growth of AS Creditinfo Eesti.

Elari joined Creditinfo in 2019 as Director IT in the Baltics, progressing to Management Board member and Head of IT Baltics. Now as CEO, Elari will be responsible for the largest and oldest credit bureau in Estonia.

In his role, Elari will work with various internal and external stakeholders to ensure the company’s approach to strategy and growth remains first class in terms of meeting customers’ expectations and needs.

Elari Tammenurm, CEO of AS Creditinfo Eesti said: “Today everyone has access to vast amounts of data; however, the abundance of data can make it more difficult to make well-informed business decisions in an ever-changing business environment. In my new role, it’s my goal to further ensure the facilitation of this process through delivering world class solutions to the Estonian market including various new Decision Analytics and Scoring related products. This will allow us to continue driving valuable and positive outcomes for our clients and enable greater access to finance and economic growth in Estonia.”

Paul Randall, CEO of Creditinfo Group, said: “With roots in financial services and IT strategy, Elari knows how to solve our clients’ unique business challenges. His knowledge of the company, our people, our industry, and our clients is a huge advantage for AS Creditinfo Eesti’s innovation and growth as we continue to expand in the Estonian market. We’re proud to have Elari leading the way.”

END

About Creditinfo

Established in 1997 and headquartered in London, UK, Creditinfo is a provider of credit information and risk management solutions worldwide. As one of the fastest-growing companies in its field, Creditinfo facilitates access to finance, through intelligent information, software and decision analytics solutions.

With more than 30 credit bureaus running today, Creditinfo has the most considerable global presence in this field of credit risk management, with a significantly greater footprint than competitors. For decades it has provided business information, risk management and credit bureau solutions to some of the largest, lenders, governments and central banks globally to increase financial inclusion and generate economic growth by allowing credit access for SMEs and individuals.

For more information, please visit www.creditinfo.com / www.creditinfo.ee

The Role of Artificial Intelligence and Machine Learning in Credit Scoring

Executive Summary

The use of artificial intelligence (AI) and machine learning (ML) in credit scoring is revolutionizing the lending industry. By leveraging vast amounts of data and advanced algorithms, lenders are able to more accurately predict credit risk, improve operational efficiency, and expand access to credit for underbanked individuals and small businesses. This white paper explores the benefits and challenges of AI and ML credit scoring, and provides guidance for lenders on how to successfully integrate these technologies into their lending processes.

Introduction

Traditional credit scoring models rely on a limited set of data points, such as payment history, outstanding debt, and length of credit history, to assess creditworthiness. These models are effective for many borrowers, but they can be limiting for individuals with thin credit files or non-traditional sources of income. AI and ML credit scoring models, on the other hand, can analyze a vast array of data points, including non-traditional data sources, to develop a more accurate and comprehensive picture of a borrower’s creditworthiness.

Benefits of AI and ML Credit Scoring:

1. Improved accuracy: AI and ML algorithms can analyze a wide range of data points, including non-traditional data sources such as social media activity and utility bill payments, to develop a more accurate picture of a borrower’s creditworthiness. This can result in more accurate credit scores and better loan decisions.

2. Expanded access to credit: Traditional credit scoring models can be limiting for individuals with thin credit files or non-traditional sources of income. By analyzing a broader range of data points, AI and ML credit scoring models can expand access to credit for underbanked individuals and small businesses.

3. Increased efficiency: AI and ML credit scoring models can automate many aspects of the lending process, reducing the need for manual underwriting and improving operational efficiency. This can result in faster loan decisions and a better borrower experience.

Challenges of AI and ML Credit Scoring:

1. Data privacy and security: As AI and ML credit scoring models rely on vast amounts of data, data privacy and security are critical concerns. Lenders must ensure that they are collecting and using data in compliance with applicable laws and regulations, and that they have robust cybersecurity measures in place to protect sensitive borrower data.

2. Bias and discrimination: AI and ML algorithms are only as good as the data they are trained on, and if that data is biased, the algorithms can perpetuate that bias. Lenders must be mindful of potential biases in their data and take steps to mitigate any potential discrimination in their lending decisions.

3. Explainability: AI and ML algorithms can be complex and difficult to interpret, which can make it challenging for lenders to explain their lending decisions to borrowers. Lenders must be able to provide clear explanations of their credit scoring models and lending decisions to borrowers.

Conclusion

AI and ML credit scoring has the potential to revolutionize the lending industry, providing more accurate credit scores, expanding access to credit, and improving operational efficiency. However, lenders must be mindful of the potential challenges, including data privacy and security, bias and discrimination, and explainability, and take steps to mitigate these risks. By investing in AI and ML technologies and developing robust risk management practices, lenders can successfully integrate these technologies into their lending processes and provide better loan decisions and a better borrower experience.

Samuel White

Director of Direct Marekts, Creditinfo Group.

ESG and the Banking Industry: Why Sustainability Matters

As the world grapples with environmental and social challenges such as climate change, social inequality, and governance failures, the importance of ESG (Environmental, Social, and Governance) considerations has never been more apparent. For banks, ESG is becoming an increasingly important aspect of doing business, as it can help to manage risks, enhance reputation, meet regulatory requirements, drive innovation and increase access to capital. In this blog post, we’ll explore each of these points in more detail.

- Risk management: ESG risks are significant and multifaceted, ranging from physical risks such as climate change-related natural disasters to transition risks stemming from legal and policy risks from greenhouse gas emissions and governance or social issues such as human rights abuses. By integrating ESG considerations into their risk management frameworks, banks can better anticipate and manage these risks, which can have a positive impact on their financial performance. For example, banks that fail to properly assess and manage climate-related risks could face stranded assets or lawsuits, which could impact their bottom line. Regulatory frameworks in Europe have taken note of this and the European Banking Authority now requires banks to disclose multiple data-points regarding ESG risks in their risk reports (Pillar III).

- Reputation: ESG is increasingly important to customers, investors, and other stakeholders who want to see banks acting as responsible corporate citizens. Banks that take ESG seriously and demonstrate their commitment to sustainability and social responsibility are more likely to attract and retain customers, as well as to access funding from ESG-focused investors. For example, a bank that invests in renewable energy projects or supports social programs in its local community is likely to be viewed more favorably than a bank that does not prioritize ESG. Mismanaging ESG factors to increase reputation may have negative effects, which became evident in some high-profile cases in 2022, both in the EU and US.

- Regulatory pressure: Regulators around the world are increasingly focusing on ESG issues and requiring banks to integrate these considerations into their business practices. For example, the European Union has introduced regulations such as the Sustainable Finance Disclosure Regulation (SFDR) and the Taxonomy Regulation, which require banks to disclose ESG-related information and align their investments with environmental objectives. Banks that fail to comply with these regulations could face fines or other penalties, which could impact their financial performance, reputation, and limit access to capital.

- Innovation: Banks that prioritize ESG are more likely to drive innovation and develop new products and services that address environmental and social challenges. By supporting the transition to a low-carbon economy and promoting social inclusion, banks can help to create a more sustainable and equitable future. For example, a bank that issues green bonds or sustainable investment products can help to finance renewable energy projects or other environmentally beneficial initiatives, potentially at better rates. Similarly, a bank that offers financial services to underserved communities can help to promote financial inclusion and social equality.

- Green bond issuance offers several benefits for banks, such as accessing a growing pool of socially responsible investors, improving their reputation as sustainable financial institutions, and supporting the transition to a low-carbon economy. The growth of the green bond market has been impressive, with a record-high issuance of $269.5 billion in 2021, up 4.6% from 2020. The cumulative issuance from 2007 to 2021 surpassed $1.5 trillion, with the US, China, and France being the largest issuers. The increase in green bond issuance is driven by investor demand and regulatory measures promoting sustainable finance.

In conclusion, ESG considerations are becoming increasingly important to the banking industry to manage risk, enhance reputation, meet regulatory requirements, and drive innovation. Banks that prioritize ESG are likely to be better positioned for long-term success, as they can help to create a more sustainable and equitable future for all stakeholders. As individuals, we can also play a role in promoting ESG considerations by supporting banks and financial institutions that prioritize sustainability and social responsibility. By working together, we can help to build a more resilient and sustainable global economy.

This may be one of the most important feature of ESG in banking, where the green bond space has grown exponentially over the last years.

By Gary Brown

Head of Commercial Development – Creditinfo Group.

Lithuanian debts increased by €6.8 million since the beginning of 2023

According to Creditinfo Lithuania’s latest analysis, Lithuanian debts have increased by €6.8 million since the beginning of the year, reaching a total of €364.8 million.

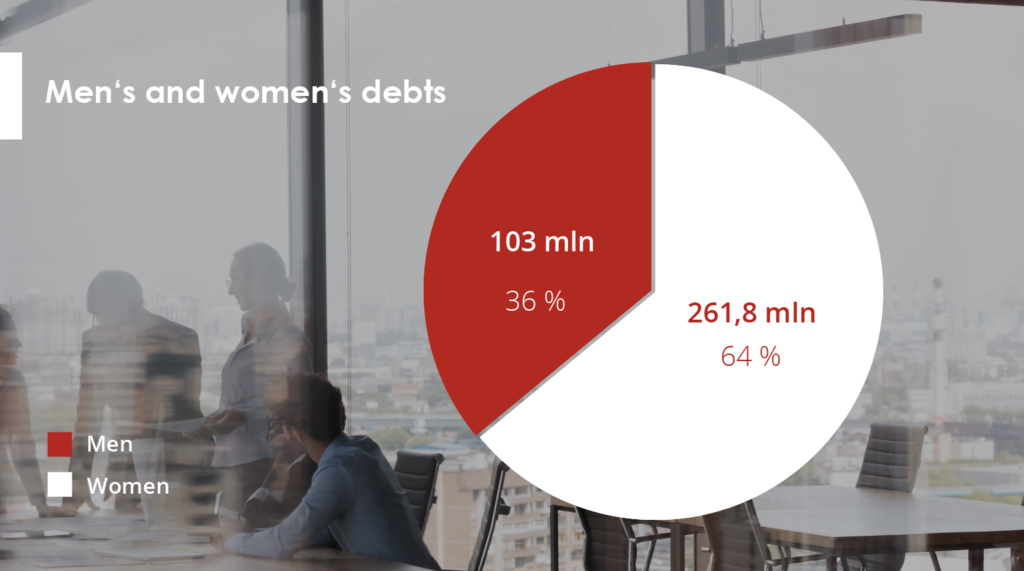

Of this amount, male’s debts stand at €261.8 million, while female’s debts are at €103 million. This is almost €6.8 million more than at the beginning of this year (€358 million). The total number of borrowers has also risen by 5,000 in the first quarter of this year, with the current total standing at almost 201,000.

Creditinfo Lithuania has recorded almost 201,000 debtors in its systems for March, with a total of 235,300 individuals having 235,300 debts in Lithuania.

After a more detailed examination of the debtor data, it was found that over 129,000 males and 72,000 females are currently in debt, making up 64% and 36% of all debtors respectively. Additionally, 32,500 males and almost 20,000 females have multiple debts, with 25.3% of male debtors and 27.7% of female debtors holding two or more debts.

On average, males owe €2,029, which is 30% more than the average debt owed by females (€1,435). This trend, coupled with the higher number of male debtors, results in men holding 78% of the total debt amount, while women hold only 22%.

During the first quarter, an additional 5,000 individuals in Lithuania fell into debt.

In March, the total number of individuals in debt amounted to 201,000, marking an increase of 5,000 from January’s 196,000. The total value of debt owed by all debtors also rose from €358 million to €364.8 million, with the total number of debts recorded in the credit bureau system increasing by 5,300. The largest number of new debts to households registered in the first quarter of this year, after debts to the financial sector, were for utilities and energy, with a total of 1,518 debts (12%).

“The analysis suggests that the majority of new debts recorded this year can be attributed to the energy and heat price crisis. Rising fuel costs have resulted in increased indebtedness, with people seeking short-term financing in order to balance consumption and expenses,” explains Aurimas Kačinskas, the Head of Creditinfo Lithuania. “Not everyone has had sufficient time to alter their financial habits, which has resulted in the growing number and value of debts.”

Men aged between 35 and 45 are considered to be the most high-risk debtors

Despite fluctuations in the number of borrowers and their levels of indebtedness, the typical borrower profile has remained consistent in recent years. Men aged 35-45 are the riskiest debtors, with debts amounting to €75 million, accounting for almost 29% of the total amount owed by men. The second riskiest group is men aged 45-55, with €61 million in debt, representing 23.3% of the total amount owed by men. In third place are men aged 25-35, who hold €55 million in debt, accounting for 21% of the total amount owed by men. Men aged 55-65 hold €43 million in debt, while those over 65 hold €17 million. Men under 25 hold the lowest amount of debt at almost €15 million.

Among female debtors, the under-25 age group has the lowest amount of debt, while other age groups have the following distribution: €29 million (45-55), €26 million (35-45), €20 million (55-65), and €17 million each (25-35 and over 65).

According to Mr Kačinskas, it is important for citizens to assume their financial obligations responsibly and meet them on time to maintain a positive credit history, which determines their access to financial services, loans, credit cards and payment provisions.

Creditinfo Partners With VisionFund International to Provide Analytics and Automation Solutions

Creditinfo Group, the leading global service provider for credit information and risk management solutions, today announces a multi-market partnership with VisionFund International to provide analytics and automation solutions throughout their global Microfinance Network.

Creditinfo’s credit risk analytics and automation solution will help VisionFund to expand their customer base whilst controlling costs. This will enable VisionFund to increase financial inclusion and improve economic conditions for lower income clients around the world.

Creditinfo will draw upon its global and regional experts to support the implementation of these solutions over a three-year period. Initially, Creditinfo will provide its solutions to six of VisionFund’s markets with a view to extending them to additional VisionFund’s markets in due course.

Paul Randall, CEO at Creditinfo said: “We are delighted to have been selected by VisionFund International to provide IDM Decision Automation solution to their global network of MFIs (Microfinance institutions). Our understanding and experience of working across over 20 markets is strongly aligned with VisionFund’s experience as one of the largest multinational networks of MFIs with its operations spanning 28 countries and reaching over 1 million active customers. We are excited about the journey ahead and helping VisionFund realize its goal of enabling clients to grow their livelihoods and secure their futures.”

Karen Lewin, Director of Credit Risk at Vision Fund International said: “With Creditinfo’s solution, we will increase our outreach, and improve both lending efficiency and our credit risk assessment capabilities, to better meet the needs of all our customers. Creditinfo’s team of global and local experts will provide us with the level of support we need to achieve these goals and increase financial inclusion in the markets where we operate.”

For information visit www.creditinfo.com

Kredītinformācijas Birojs and Citadel Bank Sign an Agreement to make It easier for Ukrainian citizens to receive Financial Services

It has already been reported that last year the “Credit Information Bureau” of Latvia (KIB) concluded an agreement with the “International Credit Information Bureau” in Ukraine ( Мидрождение бюро кредитних історий ) on the exchange of credit history data of Ukrainian nationals.

One of the safest businesses in Lithuania – Dental Services

The profitability of some companies is almost half their revenues, very few go bankrupt.

Vilnius, Lithuania 06/02/2023. Although most dental businesses are small and usually employ fewer than 10 people, this is one of the most stable businesses in Lithuania. Profitability often exceeds one-third of income and only a few become insolvent. Dental businesses are 7 times less likely to go bankrupt than the average insolvency across all other businesses, according to an analysis conducted by Creditinfo Lithuania.

According to data from January 2023, there are currently almost 2,000 dental businesses in Lithuania employing 9,500 people. The number of companies and their employees is growing year on year. Dental businesses are generally small, with more than half of them employing fewer than 10 people. Only 12 organisations have created more than 50 jobs, while the largest dental service companies are Vilnius University Hospital (293), SB Dental Clinic (168), Denticija (153), Smile Academy (126), Smile Laboratory (124), Vilnius Implantology Centre Clinic (93), Panevėžys City Dental Clinic (72), Laudenta (71), Pasirink (66) and Žvėrynas Dental Clinic (59).

Revenues grow year on year, profitability remains high

Despite the pandemic’s restrictions on the medical services sector between 2020 and 2021, the total revenue of dental companies has grown consistently year on year, reaching €294.6 million in 2021, an increase of 39.8% compared to 2020 (€210.7 million), which in turn is an increase of 76% compared to 2019 (€167 million).

The top 10 companies with the most revenue in 2021 are SB Dental Clinic (€8.2 million), Vilnius Implantology Centre Clinic (~€7 million), Denticija (€3.2 million), Smile Academy (€3.1 million), Prodenta (€3.1 million), Žvėrynas Dental Clinic (€3 million), Sveikatos Gija (€2.9 million), Šiauliai Implantology Centre (€2.8 million), Laudenta (€2.6 million) and Dental Harmony (€2.6 million).

Dental service companies are characterised by relatively high profitability, reaching up to 45%. The top ten companies with the highest profits in 2021 are Laudenta (€922 thousand), SB Dental Clinic (€917 thousand), Implantera (€739 thousand), Šiauliai Implantology Centre (€713 thousand), Smile Design (€688 thousand), Vilnius Implantology Centre Clinic (€644 thousand), Klaipėda Orthodontics Centre (€592 thousand), Dantima (€556 thousand), Donatas Jurgaicis Odontology Clinic (€529 thousand) and Teeth Centre (€512 thousand).

“The dental services business has advantages – patients usually pay for services immediately, which speeds up the turnover of funds. In addition, some dental services are subject to significant VAT exemptions, which reduces the tax burden and increases the profitability of the companies,” says Jekaterina Rojaka, Head of Business Development and Strategy at Creditinfo Lithuania.

However, not all companies were profitable, with 148 dental service providers declaring a loss in 2021, compared to 128 in pandemic year 2020 and 133 in pre-pandemic year 2019.

Dentists 7 times less likely to go bankrupt

The dental services sector has a particularly low risk of bankruptcy compared to all other sectors, with 1% of firms currently at high risk of bankruptcy and 0% at the highest risk. The high and highest risk classes for late payment are 3% and 2% of companies, respectively. The riskiness of dental firms was slightly higher at the beginning of 2021, with 4% of firms in the high bankruptcy risk class (none in the highest) and 11% in the high and highest delayed payment risk classes.

No dental companies went bankrupt in 2021 or 2022, while 26 firms have become insolvent since 2003, an average of 1-2 per year.

The dental business is characterised by a low level of debt. As of January 2023, there were 98 registered debts in the credit bureau’s system, totalling €95 thousand. The average debt was €971.

Compared to companies operating in other sectors in Lithuania, dental service companies are 7 times less risky. For example, in January this year, 1.3% of dental businesses were classified as high and highest risk, compared to an average of 9.5% for all other businesses in Lithuania. In terms of the risk of late payment, 4.5% of firms were in the high and highest risk classes, while the average for all other firms was 17.2%.

Almost a fifth of dental businesses (359) have not yet submitted their financial statements for 2021.

More information:

Jekaterina Rojaka, Head of Business Development and Strategy, Creditinfo Lithuania (jekaterina.rojaka@creditinfo.com)

Travel agencies in Lithuania are slowly rising from the ashes

Revenues doubled in a year but remained three times lower than before the pandemic.

Vilnius, Lithuania, 24/01/2023. Travel agencies in Lithuania that declared their income in 2021 earned almost twice as much as in the previous year. However, compared to income in 2019, they earned almost three times less, according to an analysis carried out by the credit bureau Creditinfo Lietuva. Almost 100 tourism companies were loss-making. With the increase in travel flows, the number of debts increases and their average size grows.

There are currently 783 companies in Lithuania for which tour organisation is the main activity. In 2021, travel agencies declaring revenues collectively earned more than €171 million, almost double (82%) the pandemic year 2020 (~€94 million). However, travel agencies are still a long way from a real recovery – for example, in 2019, their revenues were almost €474 million, but fell more than fivefold in the aftermath of the pandemic.

According to 2021 data, the largest annual revenue was earned by the following companies: Novaturas (€108,995 million), Tez Tour (~€60 million), Itaka Lietuva (€12.5 million), Coral Travel Lithuania (€9.5 million), Kidy Tour (€8.9 million), Estravel Vilnius (€6.3 million), Estekspress (€4 million), Traveldeals LT (€4 million), Glotera (€3.6 million) and ZIP Travel (€2.9 million).

The top ten most profitable travel agencies are Novaturas (€909 thousand), Baltic Tours Group (€633 thousand), Vestekspress (€530 thousand), Glotera (€336 thousand), Traveldeals LT (€307 thousand), Baltic Clipper (€288 thousand), Baltic Travel Service (€271 thousand), TEZ Tour (€215 thousand), Estravel Vilnius (€158 thousand), Riviera Tours (€148 thousand) and ZIP Travel (€123 thousand).

Staff numbers shrink by a quarter

In total, travel agencies currently employ almost 2,000 employees (1,850). While the number of enterprises has remained almost constant over the past few years (776 in 2019, 787 in 2021), the number of employees has fallen by almost a quarter since 2019, from 2,426 to 1,850.

Travel agencies are more often headed by women, accounting for almost 56% of all managers. The average age of a travel agency manager is 49 years and the average age of a travel agency is over 15 years.

In the travel sector, men’s salaries are higher than women’s – as of November 2022, the average salary for men was €2,659 per month, while for women it was €2,014 per month. At the start of 2022, the average salary for women was €2,053 per month and for men was €2,364 per month.

State support has prevented more bankruptcies

Since 2004, a total of 94 travel agencies have gone bankrupt in Lithuania, with the highest number of bankruptcies recorded in 2009 (10) and in 2015 (12). In 2022, there were 5 travel agency bankruptcies, while there were 3 in 2021 and 4 in 2019. No travel agency bankruptcy was recorded in pandemic year 2020.

“The travel sector was one of the hardest hit by the pandemic, along with hotels and restaurants. During the pandemic, when revenues from tour operators dropped fivefold, it was state support that saved the sector from bankruptcy,” explains Aurimas Kačinskas. But the challenges of the pandemic were replaced last year by new challenges – the war in Ukraine and the sanctions imposed on Russia have exacerbated the energy crisis, fuel prices have risen and many travel routes have been disrupted. The slower-than-expected recovery of the air transport sector, with a sharp increase in fares, is having a negative impact on the business of tour operators, preventing them from recovering faster.

According to the head of the credit bureau, it was state support that determined the stability of the number of enterprises and the discipline of submitting financial statements – compared to other sectors, only 90 travel agencies did not submit their financial statements for 2021, making them ineligible for state support.

However, a risk analysis of travel agencies shows that there have been both positive and worrying signs in the recent period. For example, as of January this year, 9% of companies were in the high and highest classes of bankruptcy, compared with 12% a year ago. In terms of delayed payments, 17% of companies are currently in the high and highest risk classes, down from 21% last year.

Compared to 2020 and 2021, the recent increase in debt is slightly higher and the average amount of debt per person is growing. At present, 306 debts have been registered in the credit bureau system, amounting to more than €349 thousand, with an average debt of €1,141. A year ago, the number of debts was 316, amounting to €351 thousand, with an average debt of €1,112. In January 2020, 255 debts amounting to €203 thousand were registered, with an average debt of €798. 335 travel agencies mostly owe money to Sodra (€3 million). The debt of 158 travel agencies to telecommunications companies amounts to €222 thousand. 8 travel agencies owe €74 thousand to financial companies.

“The tour operator business is recovering, but revenue growth is slower than expected in the wake of the pandemic due to the many geopolitical and economic shocks around the world. The tourism sector is currently encompassed by a number of risks, so it is advisable to keep a close eye on the changing financial indicators of partners organising the trips,” concludes the head of the credit bureau.

More information:

Aurimas Kačinskas, CEO of Creditinfo Lithuania (aurimas.kacinskas@creditinfo.com)